As a part of the FInnov@teHUB, the Fluid Ice Foundation aims to empower all with the knowledge and resources to leverage FinTech services & technologies essential for achieving financial well-being.

We review FinTech services & technologies, considering cost, ease of access, & ease of use, essential for jumpstarting your financial journey.

They offer traditional banking products and services, but at considerably lower costs compared to incumbents. They can afford to do so by cutting out manual tasks and intermediate players using technology. Typical examples are remittances (money transfers) and peer-to-peer lending, with newcomers side-stepping traditional financial services companies.

The Atomizers

They atomize incumbent banks’ products that have minimum price thresholds that are too high for many to access. They do away the minimum thresholds completely or run at only a fraction of them. Example offerings include microcredit, microinsurance, microsavings, micro-pensions, micro-investments (also called fractional trading) and low-cost “robo-advisors.”

The Snipers

Sniper FinTech's offer products addressing a specific customer need or a niche, including loan advances, specific mobile payments or partial salary-taking (for example: if you have already worked five days in a given monthly paycycle, you can receive one-sixth of your monthly salary). Examples: Wagestream, M-Pesa, and BitPesa.

The Amplifiers

These companies expand access to existing financial products to a larger audience via more advanced risk-calculation techniques. They offer personalized products and services, avoiding merely considering financial factors but also including, for instance, social and psychological ones. The offerings can help people to improve their credit.

– World Economic Forum

The Educators

Simplify the understanding of existing financial products through more intuitive user experiences, greater transparency on costs and financial risks, and clear(er) explanations and training on the offered products. It strengthens customers’ skills in managing their financial affairs—encouraging them to save more and handle their money better.

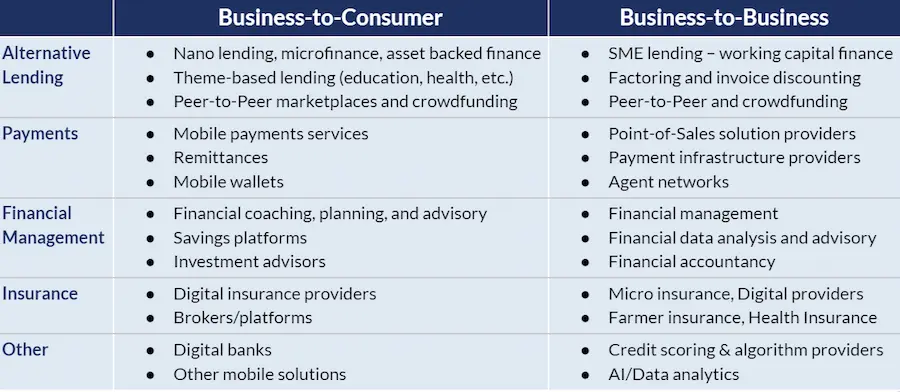

Overview of Key FinTech Sectors

The FinTech ecosystem is large and constantly evolving with new innovations, with a potential to deepen the impact of financial inclusion, strengthening our continued commitment to Project FInnov@teHUB. We truly believe that FinTech is a game changer for financial inclusion.

Fintech has the power to impact lives in a meaningful way. Through the FInnov@teHUB, we continue to strengthen and support this expanding area of financial inclusion: companies that contribute to a sustainable society through their

products, services, and business practices.

FinTechs: a digital revolution in Financial Inclusion

There are more than 12,000 fintech startups worldwide, of which 8,775 are in the Americas. Global investment in FinTech has grown to $210 billion in 2021. The global FinTech market is projected to grow to $31.5 billion by 2026, and the global financial services market is projected to reach $26.5 trillion in 2022, in which FinTechs will play a critical role. The global value of digital transactions is predicted to increase from $1.9 trillion in 2021 to $6.8 trillion by 2026.

The Global Stage

There are 188 FinTech unicorns globally, of which 100+ are in the US.

Globally, the number of smartphone users is expected to reach 7.5 billion by 2026.

Globally, digital payments expected to reach $3 trillion in transaction value by 2030.

46% of today’s consumers exclusively use digital channels for their personal banking.

Per a PwC study, globally, 88% of financial institutions believe that part of their business will be lost to standalone fintech companies in the next five years.

In Sub Saharan Africa, by 2025, there are projected to be 614 million unique mobile users (a penetration rate of 50%) and 475 million mobile internet users (a penetration rate of 39%).

African FinTech Investment surpassed $2 billion in 2021, the highest ever, a growth of $1.49 billion from the previous year.

Per GSMA, in 2020, Sub-Saharan Africa had the largest amount of mobile money transactions at $490 billion, 374% higher than the 2nd largest market, South Asia.

At 87%, India has the highest FinTech adoption rate in the world, compared to the global average of 64%.

In India, investment inflow in the Fintech sector has gone up to $10 billion.

There are ≈2,100 FinTechs in India, of which many are unicorns. India’s FinTech market is currently valued at $31 billion, & expected to grow to $84 billion by 2025.

The value of digital payments in India is expected to grow from $300 billion in 2021 to $1 trillion by 2026.

India had 25.5 billion real time payment transactions in 2020, highest in the world.

FinTechs improving financial inclusion globally

Financial Inclusion 1.0: refers to the late 1970s when microcredit developed into a proof of concept that poor and low-income households are bankable. Financial Inclusion 2.0: refers to the 1990s when microfinance institutions became scalable and commercially viable through information technology and back-office automation. Financial Inclusion 3.0: refers to FinTechs playing a critical role in increasing outreach exponentially, keeping our focus on the low-income segment, the un/underbanked and micro, small, and medium sized enterprises (MSMEs).

Increasing Access

In the US, there are 1,214 bank deserts with no physical financial institutions within a 10-mile radius, which FinTech will help mitigate through increased and easier access.

FinTechs have played a significant role in 1.1 billion previously unbanked adults gaining access to financial services in the last decade.

Reducing the MSME Gap

In developing economies, MSMEs utilize microloans for capital they need to get started and maintain their operations, enabled by FinTechs.

MSMEs are crucial in the developing world – such as Sub-Saharan Africa, where they comprise 90% of all businesses. FinTechs are able to cater to the needs of these enterprises and better serve their financial needs, to help bridge the financial inclusion gap.

Digital Payments

Globally, digital payments are expected to reach $3 trillion in transaction value by 2030.

In India, digital payments industry is expected to contribute ≈15+% to the country’s GDP, and is expected to grow to $1 trillion by 2026.

Digital payments will overall improve the global economy, and help improve the GDP of respective countries, especially in developing ones.

Lowering Costs

In Kenya, FinTechs helped lower costs of digital salary payments/wage transfers, leading to income raise up to 30% for rural households.

Annual remittances in Africa amount to $40 billion, which accounts for up to 30% of the GDP in some countries. However, the cost of these money transfers is the highest in the world, and mobile wallets using FinTech have helped lower these fees.

Globally, chatbots will save banks $7.3 billion by 2023, and AI will save the insurance industry nearly $1.3 billion by 2023.

Improving Competition

Increased competition from FinTech’s has put enormous pressure on traditional banks and financial institutions, leading them to innovate and improve the efficiency of their processes and reduce operating costs to stay relevant and profitable.

77% of traditional financial institutions plan to increase their focus on innovations to boost customer retention.

Access to Credit

A report from NYU Stern found that a consumer’s mobile and digital footprint was a better predicting factor for loan decisioning than a traditional credit score, made possible by FinTech.

FinTechs (ex: Upstart & Zest.ai) are developing inclusive models & underwriting processes to provide loans using non-traditional variables.

FinTech solutions have definitely altered the slow course of financial inclusion globally, resulting in extremely positive changes, but there is still a long way to go.

FinTech can be extended beyond finance, and translate into important changes in other areas, such as infrastructure, agriculture, development, and economic growth, which also impact financial inclusion.

Key factors affecting FinTech growth/adoption

Security/Consumer Trust: Data security has become one of the largest concerns in the digital world. Many FinTech’s require customers to provide personal information, which customers are rightfully wary of sharing. It is important that FinTech’s work to establish their security standards to help customers feel more comfortable.

Public Policy and Regulation: Finance and technology are some of the most regulated sectors, and there will always be proper steps that need to be followed, which can be hard for emerging FinTech’s to stay on top of.

Limited Access: FinTech relies on technology, whether through phones, or computers, which many people are unable to access. In the US, nearly 1 in 4 households does not have Internet access, and globally, 47% of the population do not. Additionally, it is estimated that globally 1.1 billion people do not have access to electricity, and consequently cannot use a phone, computer, or any technology.

Lack of Financial Literacy and Awareness: The lack of financial literacy has meant that a number of potential consumers are unaware of the several existing FinTech services and the extent to which they could be beneficial/used.

In the wake of FinTech super apps seamlessly providing a wide range of financial services across geographical boundaries, it is likely that the role of traditional banks will be reimagined on the global stage, led by the shift towards FinTech, while empowering financial inclusion.

We are looking to partner with innovative FinTechs!

If you are a FinTech and share our mission of sustainable innovation and are impacting financial inclusion through your products and services, we want to partner with you to further our common goals.

Vijay is the Banking and Capital Markets Leader for Deloitte South Asia. He has over 25 years of consulting experience spanning strategy, business planning, organizational transformation and M&A in India, as well as in Canada, the UK and South East Asia. Among other topics in banking and capital markets, he has significant experience in fintech solutions and related partnership models.

Vijay is also a founding team member of I_Imagine_India, an India-based philanthropic fund looking to empower non-government organizations and social entrepreneurs/pioneers in the field of education in India. I_Imagine_India’s goal is to enable small changes today in the field of primary/ pre-primary education, with the potential to deliver disproportionate learning outcome improvements over the longer term.

Vijay obtained an MBA from the Indian Institute of Management, Ahmedabad (PGPX) and the Chartered Financial Analyst (CFA) charter from the USA.

Vijay is an Advisor to the Fluid Ice Foundation in his personal capacity and not on behalf of Deloitte or I_Imagine_India.

Saiprasad Muzumdar, Advisor

Saiprasad ‘Zoom’ Muzumdar, is an experienced Senior Technology Leader in International Banking and Finance Sector. He has a Bachelor’s degree in Engineering and a Master’s degree in Management. He has worked across the globe for International Fortune 500 companies such as Unisys, Citigroup, Lehman Brothers, Nomura, Royal Bank of Scotland/NatWest Group. He has conducted sessions on Financial Wellbeing for more than a decade with a mission to enhance financial inclusion and financial wellbeing through Financial literacy.

Raj Mehta – Financial Education Instructor

Subjects/Topics Taught (1-on-1 Session):

FinVerse Academy

Financial Literacy

FinTechs

Macroeconomics

Quantum Academy

K-12 Math

SAT/ACT Math

Math Competitions

Computer Science

Linguistics Academy

English

Spanish

Hindi

Gujarati

Music and Arts Academy

Alto Saxophone

Tenor Saxophone

Virtual sessions conducted on Webex

Amit Pandit, Advisor

Amit is a qualified chartered accountant with over 25 years of experience in banking, financial services, capital markets, risk advisory services & financial education. He has experience in building a primary market distribution network, investment banking and handling HNI relationships. He has been involved in personal finance restructuring of many individual businessmen. He has helped many business and individuals for their financial requirements be it for loan arrangements or debt management or asset management. He served as a director of the largest coop bank in India for over 13 years and as a director of a listed company for over 5 years.

He is also associated as a visiting faculty with various business schools for over a decade and takes up subjects of Personal Finance Planning, Wealth Management, Mergers & Acquisitions & Corporate Valuation. He also takes corporate training programs for finance. He speaks at various platforms on various finance, audit and risk related topics including ICAI, BCAS etc. Amit looks after the business building, financial & investor education function at Trugrow.

Amit enjoys his reading, is passionate about his teaching, likes travelling and exploring new destinations and is an avid foodie.

Raj Mehta, Founder & CEO

Raj Mehta is the Founder and CEO of the Fluid Ice Foundation. As a high school student in the Atlanta metro, Georgia, Raj always enjoys helping others, and aspires to give back to society at every opportunity that comes along. Raj is particularly passionate about financial inclusion, to expand access to financial services to the un/underbanked subsets of the population. Although the un/underbanked subsets of the population have always been excluded, the recent COVID pandemic has made it even more apparent, and caused them to be even further left behind. Raj sees himself as a “social impact catalyst” and a “changemaker” to help mitigate the financial divide, and he aims to make this a reality through his nonprofit – Fluid Ice Foundation. Raj is also a financial education instructor helping increase financial literacy awareness and education, especially amongst the underprivileged youth.

Raj is focused to be a social impact entrepreneur/innovator, championing sustainable innovation by transforming societal assets/capital to enable disruptive solutions providing a positive return to society.

On a more personal note, Raj enjoys mathematics and has won numerous prestigious math competitions (qualified to Mathcounts Nationals to represent the State of Georgia, AIME, AMC, etc.), is a proficient saxophonist (member, Georgia Music Educator’s Association (GMEA) Allstate Band), is an advanced chess player, and a professionally trained/skilled golfer. He is also an avid book reader in his spare time.